Welcome

It is an honor to serve the Legislature and the citizens of the State of Florida as Auditor General and I consider it

a tremendous privilege to lead our staff of highly dedicated and qualified professionals. As the State’s independent auditor,

our mission is to provide unbiased, timely, and relevant information that the Legislature, Florida’s citizens, public entity

management, and other stakeholders can use to promote government accountability and stewardship and improve government operations.

We are dedicated to our core values of integrity, accountability, independence, and objectivity and perform audits and other

engagements in accordance with generally accepted government auditing standards as set forth by the Comptroller General

of the United States in Government Auditing Standards. More information about the audit process is available in

our Guide to Audits.

Thank you for visiting our Web site. I hope you are able to find helpful information and learn more about who we are

and what we do. If you have any questions or wish to provide your input on matters related to governmental entity accountability

and stewardship in Florida, please feel free to contact us directly.

Sincerely,

Sherrill F. Norman, CPA

, Auditor General

Our Organization

Auditor General Sherrill Norman is assisted by three Deputies and over 300 employees organized into three divisions: the Audit

Innovation and Support Division, the Educational Entities and Local Government Audits Division, and the State Government Audits

Division. The divisions are supported by a general counsel and quality control group.

Click on each division in the chart to view the division’s organizational structure.

EDUCATIONAL ENTITIES AND LOCAL GOVERNMENT AUDITS DIVISION

Greg Centers is the Deputy Auditor General of this division which has three Audit Managers:

- Ted Waller - Audit Manager of District School Boards

- Jaime Hoelscher - Audit Manager of Colleges, Universities, and Water Management Districts

- Heidi Burns - Audit Manager of Information Technology Audits - Educational Entities

This Division performs audits, including information technology audits, of school districts, State universities, State colleges, and certain other governmental entities. Audits are designed to determine whether financial resources are properly accounted for; public officials comply with applicable laws, rules, regulations, and other legal requirements; proper and effective internal controls are in place over entity operations, data, and information technology resources; and assets are properly safeguarded. Audits are conducted based on statutory requirements and risk assessments of entity operations and programs. This Division has locations in Tallahassee and throughout the State of Florida.

STATE GOVERNMENT AUDITS DIVISION

Matthew Tracy is the Deputy Auditor General of this division which has six Audit Managers:

Karen Van Amburg, Melisa Hevey, Joshua Barrett, Samantha Perry,

Brenda Shiner, and a current vacancy.

This Division performs audits of State agencies and the Judicial Branch, including information technology audits and the Statewide financial and Federal awards audits. Audits are designed to determine whether financial resources are properly accounted for; public officials comply with applicable laws, rules, regulations, and other legal requirements; proper and effective internal controls are in place over entity operations, data, and information technology resources; and assets are properly safeguarded. Audits are conducted based on statutory requirements and risk assessments of entity operations and programs. This Division is located in Tallahassee.

AUDIT INNOVATION AND SUPPORT DIVISION

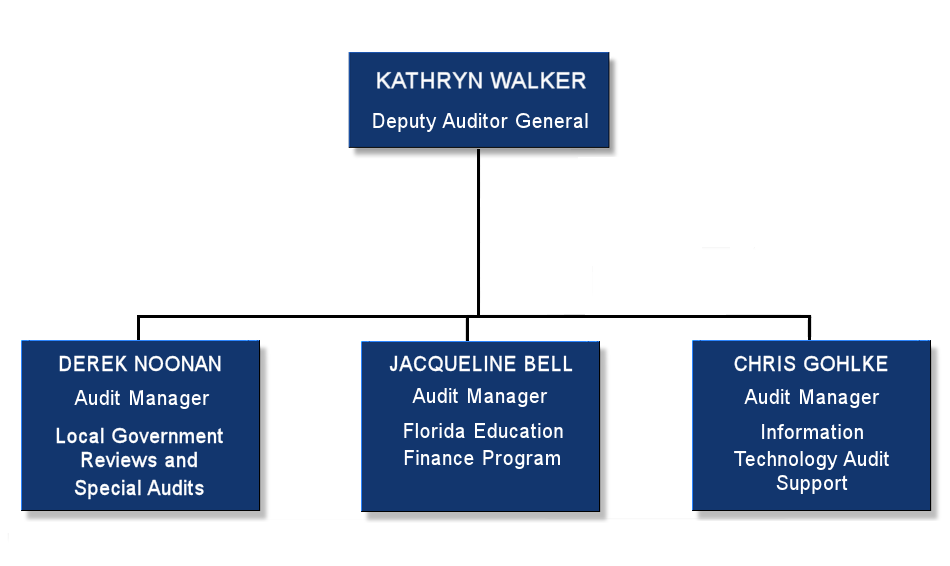

Kathryn Walker is the Deputy Auditor General of this division which has three Audit Managers:

- Derek Noonan - Audit Manager of Local Government Reviews and Special Audits

- Jacqueline Bell - Audit Manager of Florida Education Finance Program

- Chris Gohlke - Audit Manager of Information Technology Audit Support

Audit staff in this Division conduct audits of local governmental entities, examinations of school district and other entities’ records to evaluate compliance with Florida Education Finance Program (FEFP) requirements, and reviews of audit reports, including Florida Single Audit Act reports, submitted by local governments and other entities. Staff in this Division also provide audit assistance and data processing support to all three divisions. These staff are trained in the technical areas of information systems, such as programming and systems design, and in information technology audit procedures and techniques. Staff utilize state-of-the-art computer hardware and software including database, data communications, and multiple high-level programming languages. Division staff are primarily located in Tallahassee; however, FEFP auditors are located throughout the State of Florida.

Our Annual Report

These reports provide a brief description of our Office and a summary of the audit and other accountability activities

we performed during a designated 12-month period. The audits and other accountability activities include assignments made

to our Office both in law and by legislative directive. Each year, our dedicated team of audit professionals and support

staff generally issue over 200 reports related to operational, financial, and Federal awards audits and attestation examination

engagements of State and local governmental entities.

Prior Years Annual Reports:

- November 1, 2023 – October 31, 2024

- November 1, 2022 – October 31, 2023

- November 1, 2021 – October 31, 2022

- November 1, 2020 – October 31, 2021

- November 1, 2019 – October 31, 2020

- November 1, 2018 – October 31, 2019

- November 1, 2017 – October 31, 2018

- November 1, 2016 – October 31, 2017

- November 1, 2015 – October 31, 2016

Our History

Since 1969, the Auditor General has been the State of Florida’s independent auditor. However, the Florida

Legislature has provided for an audit function since Florida became a State in 1845.

The first legislative session after Florida’s admission to the Union in 1845 established legislative oversight

of governmental operations by requiring a joint legislative committee to examine the comptroller’s office and

the accounts of the treasury during each session. State law subsequently granted the Governor oversight authority,

which, in 1899, included the power to appoint an expert agent to examine the books, vouchers, and records connected

with the office of any State official. The law also charged the Governor with causing an examination of all

State officials who handled State funds once every 2 years and providing the results of the examinations to

the Legislature.

In 1901, State law required the Governor to appoint another agent, qualified as an expert accountant, to

examine the accounts and records of all county officers. The Expert Accountant was instructed to issue the report

to the Governor and the county commissioners. The 1903 Legislature repealed the provisions establishing the

positions of expert agent and expert accountant and established the position of the State Auditor, consolidating

the duties of the two preceding offices. Under this law, the Governor was charged with appointing a State Auditor,

who was qualified as an expert accountant, to examine the books of accounts, records and property held by State

and county officers and to ascertain the accuracy of such records. The State Auditor’s duties included reporting

the financial condition of each cabinet office to the Legislature during session.

The 1921 Legislature abolished the position of State Auditor and transferred the office’s functions, property,

and records to the State Comptroller’s office. However, in 1927, the Legislature created the State Auditing

Department, which consisted of the State Auditor and ten assistant auditors, all appointed by the Governor.

The law authorized the State Auditor to make and enforce rules and regulations necessary to facilitate proper

audits and required the annual audit of all State and county officers, state institutions and state boards and

departments.

The 1943 Legislature addressed the need for additional auditing of counties by authorizing the Governor,

upon the request of the board of county commissioners of any county with a population in excess of 50,000, to

detail an Assistant State Auditor for continuous service in such county. The Auditor, who was paid by the requesting

county, was to examine and audit the offices, books, records, and accounts of all county officials, boards and

other public institutions, except municipalities, within the county.

In 1955, the Legislature created the Legislative Auditing Committee as a joint legislative standing committee.

The Committee’s responsibilities included periodically meeting with the State Auditor, reviewing the work of

the State Auditing Department, and providing the Governor a list of candidates eligible for appointment as State

Auditor. The Committee also had the authority to direct the State Auditor to make a special audit of any entity

subject to audit. This Act recreated the State Auditing Department, required that the State Auditor be a

certified public accountant, established that the State Auditor could be removed only for cause, and made the

position subject to Senate confirmation.

The 1967 Legislature created the position of Legislative Auditor who was employed by the Legislative Auditing

Committee. The Legislative Auditor was granted the duties, personnel, and property formerly possessed by the

State Auditing Department. While the statutory provisions governing and creating the State Auditing Department

were not repealed until 1969, the Department ceased to function after the creation of the Legislative Auditor.

The 1968 Revision to the Florida Constitution created Article III, Section 2, which provided in part that

the “Legislature shall appoint an auditor to serve at its pleasure who shall audit public records and perform

related duties as prescribed by law or concurrent resolution.” In 1969, the Legislature repealed the law creating

the Legislative Auditor and enacted Section 11.41, Florida Statutes (1969), indicating the auditor appointed

by the Legislature under the constitution is designated the Auditor General. Since 1969, the auditor for the

State of Florida has been the Auditor General.

Since the appointment of the first Auditor General, the Legislature has at various times modified the scope

of the Auditor General’s authority, duties, and responsibilities. The core function, however, of being the independent

auditor for the State of Florida has remained unchanged. The Auditor General continues to be appointed by and

serve at the pleasure of the Legislature.